No. of views : (8039)

What is SGST, CGST & IGST?

Posted on: 14/Jul/2017 2:12:45 PM

For all Goods and Services, the Goods and Services Tax or GST will be imposed. This is a replacement for all other kinds of taxes. This brings all the taxes under one roof and make things easier. The below taxes will thus get replaced:

- Taxes imposed by the centre

- Service tax

- Central Excise duty

- Additional Duties of Customs or CVD

- Special Additional Duty of Customs

Taxes imposed by the state

- State VAT

- Central Sales Tax

- Entertainment and Amusement tax

- Taxes on lotteries, betting and gambling

Why are SGST, CGST and IGST imposed?

In India, both the centre and state have got the authority to levy and collect taxes. As per the constitution of either of the levels of government, there are distinct responsibilities with each of them. This requires raising resources. Hence, with dual GST, it will be possible to keeping up with the constitutional requirement of fiscal federalism. There will be GST imposed by the centre and state simultaneously.

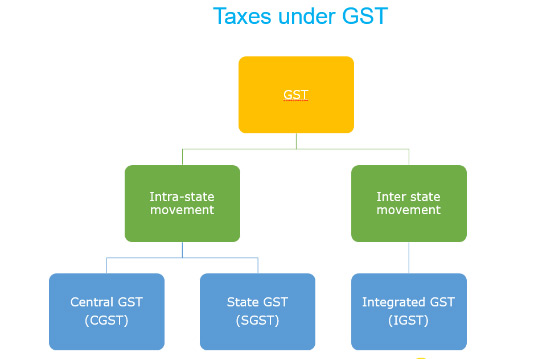

What is SGST, CGST and IGST?

CGST is Central GST. This is nothing but the GST imposed by the centre towards intra-state goods or services supplied. Similarly, the tax imposed by the state is called SGST.

The centre collects Integrated GST called IGST towards inter-state supply of goods or services. IGST is also imposed on imports.

GST is basically a composition based tax. In other words, GST can be implemented by the state where the goods or services are acquired, and not in the state where goods get manufactured. With IGST, we can ensure seamless input tax credit between states. For settling tax amounts, a state has to deal only with the centre and not the other states. So, ultimately, the overall prices is simple and easy.

Example, if a dealer in Punjab sells goods to a person in the Punjab of worth Rs 10,000, the GST is 18%. This includes 9% of CGST and 9% of SGST. So, the dealer collects Rs 1800 of which Rs 900 will reach the hands of central government and Rs 900 will go to the Punjab government.

On the other hand, if the dealer in Punjab has sold goods worth Rs 1,00,000 to a person in Gujarat, the GST will be 18 percent of which CGST is 9 percent and SGST is 9 percent. So, here, the dealer ought to impose Rs 18,000 as IGST. And the entire IGST will reach the hands of the centre.

For example, if a manufacture (dealer a) in Maharashtra sells Rs 10,000 worth goods to another dealer in Maharashtra itself (dealer b), and if this dealer b sells the same to a trader (dealer c) in Rajasthan for Rs 17,500, and this dealer c in turn sells the same to the end user in Rajasthan for Rs 30,000.

The CGST imposed is 9% and SGST is 9% and hence IGST is total of 18%. Between dealer a and b, the deal gets over within the same state and hence the CGST is 9% and SGST is 9%. Whereas with dealer b and dealer c, it is interstate and hence IGST will be 18%. Now again, the dealer c sells the good to end user within the same state and hence the CGST and SGST will both be 9%.

The IGST will be first of all imposed on IGST and then CGST. The rest will be for SGST.